Special Report: Attractive TSX-V markets

“A market that’s down by 90 per cent is exactly 90 per cent more attractive than it was before.”

— Rick Rule, Sprott Global Resource Investments, Ltd. Toronto.

During the first 10 years of the new millennium, the commodity sector rode the rapids of one of the greatest bull markets ever. Gold, silver, oil, copper, and more all set enormous record highs.

Along with those highs, came a frenzy of activity as huge resource companies went on an acquisition spree to bulk up their portfolios of high priced assets. Mid-tier and small resource companies scrambled to gather up and advance projects that demonstrated new economic potential based on rising commodity price levels.

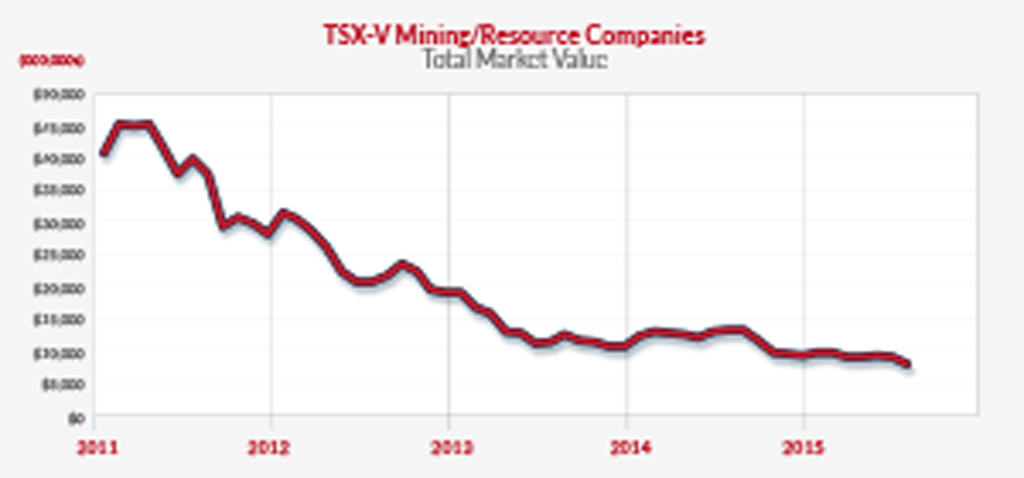

Performance of TSXV-V mining and resource companies.

During 2011, however, it became evident that the good times could not last forever. As metal prices began to level off and drift down, mining companies saw their profit expectations reverse and their market value begin to evaporate. What were once high valued assets were being written off and large scale projects were halted. Share performance and market capitalization for the world’s largest miners began to slide and it has been calculated that these major mining companies, which include such names as Glencore, BHP Billiton, Anglo American, Exxon Mobil and Barrick Gold, have collectively lost approximately $1 trillion CDN in equity value over the last 5 years.

In relative terms, the backlash on the Junior Resource sector was even worse. The collective market value of the 1,200 metals, mining and exploration companies on the TSX Venture Exchange fell from a peak of over $45 billion in early 2011 to its current level of $8 billion – a staggering 82%. If you remove the top 100 companies, that number approaches 90%.

“The current metals and mining market is crushed,” said Michael White, President and Chief Executive Officer of IBK Capital Corp., an independent and privately owned investment banking firm based in Toronto. “As in 2000, however, we are once again looking at a very attractive entry point for investment.”

“For example,” says White, “you can buy stock in a non-producing gold resource company with quality assets for $2 to $3 per ounce of gold resource in the ground. The average paid by companies in the last eight years to buy these types of ounces is just over $40 per ounce and can be higher than $100 per ounce. Undoubtedly, values will eventually return to those levels as we come out of this cycle, but investors must do their homework before stepping in.”

The challenge stems from the care required to identify those companies that will be able to advance during these difficult times and position themselves properly to skyrocket when values return. White identifies three key variables.

Assets

First and foremost, does the asset make sense in the existing economic climate? If it is a producing mine or if it is in development, can it be profitable at current commodity prices? With uncertainty as to when the resource sector may turn around, it is important to ensure that the company can operate or even thrive within today’s economic reality.

In the case of an exploration asset, that assessment is even more difficult. In a market where well defined assets have lost most of their value, an exploration opportunity can be a very high risk proposition. “The right exploration assets, however, can also provide some of the greatest opportunity”, says White, “but they must have the potential to be world class deposits and must have the ability to continue funding exploration, even a modest level”.

“If the economics work today, they will be spectacular in better markets”.

People

The quality of an asset alone, does not create an opportunity. It requires the right set of skills and expertise to deliver on a quality value proposition. Have they built mines before, have they worked in the target jurisdiction before, have they made real discoveries in their past, do they have the flexibility and ingenuity to adapt to a changing environment?

“We won’t make an investment without the confidence that there is a first class team we can rely on. It is the single most important factor we look to”, says White.

Strategy “

You need to avoid companies with no business plan. Doing nothing until the bull market returns is not acceptable”.

Companies should be able to demonstrate sustainable cash flows or a logical path to cash flows. In the case of exploration they need to have a clear plan and funding strategy possibly through strong joint venture partners or solid long term investors.

More aggressive companies are looking for opportunities to pick up additional assets during this time of low prices. Such companies will come out of this cycle looking very different than they do today.

Two examples that tick all of the boxes are Toronto-based Minera Alamos Inc. developing their copper project in Mexico and Vancouver’s TriMetals Mining Inc. with their gold-silver exploration project in Nevada/Utah, USA.

The team at Minera Alamos has been building and operating mines together in Mexico for over 10 years. When the markets began tightening up, the team made three key changes to their project plans. They started by re-designing the size of their operations reducing their construction costs to between $8-10 million, or about 10% of their original plan. Second, they defined a high grade starter pit within their already high grade resource, taking the grade of the rock from approximately 1% copper equivalent grade to closer to 2% copper equivalent grade.

Finally, they evaluated the use of sensor based ore sorting in their process. By using an x-ray transmission (XRT) sorter to pre-concentrate the ore, they hope to double the grade to about 4% copper prior to mill processing.

“In the end, we hope to make a small mine deliver cash flows like a medium sized mine, all for a fraction of the original price. The economics are quite spectacular,” says CEO Chris Frostad.

“And investors appreciate the new approach. On the back of this new plan the company was able to raise $3.5 million. We are now quickly looking for additional projects to fill out our Mexican portfolio.”

TriMetals is another junior resource company positioned well for these times. Through careful advancement, and the backing and support of a strong shareholder base, they have been able to demonstrate the potential of defining a 3-5 million ounce gold resource.

Discoveries exceeding 3 million ounces of gold are rare, and on average, over the last 10 years, there have only been one per year. This compares to five per year over the 10 years prior to that.

The TriMetals team has defined close to 1 million ounces of gold now and can show that they have only touched the surface of the area’s potential size.

Mike White believes that “Tremendous money will be made by those who purchase good quality metals assets here at the bottom of the cycle and we believe, because prices are so cheap, shares in these companies will concentrate in relatively few hands. That is to say, as we emerge from this cycle, share floats will be tight, producing conditions that could see these junior stocks gap up in steps. Those early gains will be breathtaking – a 5 cent stock will move to 50 cents seemingly overnight. The next step could be to $1.00. We want to be an owner before the five times lift to ultimately see 10 times rather than buying later for a two times lift.”

“Moreover, not all junior mining stocks will move together.

Some companies will benefit earlier than others. You want to be an owner in companies that take advantage of a disconnected market to grow by acquisition. It is happening now and some of these companies will become the rising stars of tomorrow.”

Information for this article provided by Michael White, President and Chief Executive Officer, IBK Capital Corp., Toronto.

Comments