Related Posts

April 1, 2026

Brokk hires first dedicated service manager for Canada

JV: Orix mines historical data to support mines of the future

Paragon Labs launches fast-track assay service in BC

April 1, 2026

Paragon Labs launches fast-track assay service in BC

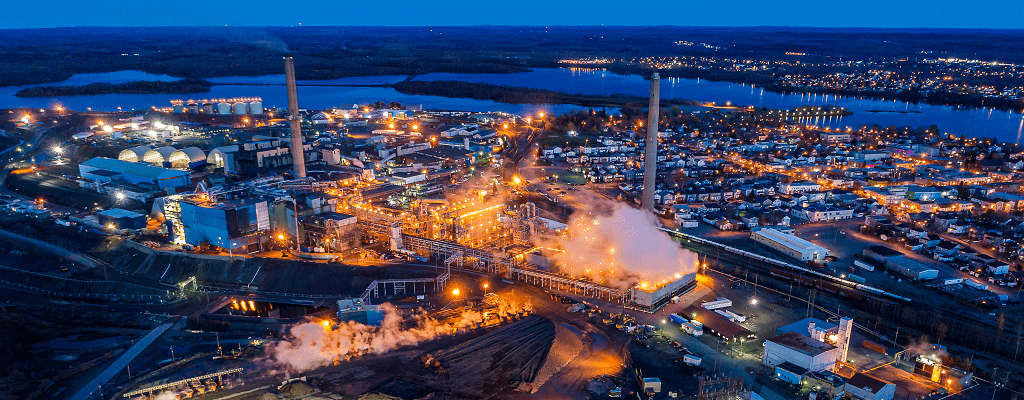

Glencore seeks Canada funding for copper smelter

April 1, 2026

Glencore seeks Canada funding for copper smelter

Comments