The fight for control of the Cerro Negro gold project in Argentina appears to have been short and sweet. No sooner had Endeavour Gold Corp. of Vancouver made a $3.4-billion offer to acquire the project owner, Andean Resources of Salt Lake City, UT, than another Vancouver company, Goldcorp, jumped in with a $3.6-billion offer.

Goldcorp's successful move shouldn't be a surprise. The CEOs of both companies, Charles Jeannes at Goldcorp and Wayne Hubert of Andean, have worked together before. Bonanza grades and the completion of a feasibility study make Cerro Negro very appealing.

Goldcorp considers Cerro Negro a great asset to have in its pipeline of new mines. The project, located in the Santa Cruz province in southern Argentina, is a low-sulphidation, epithermal gold deposit hosted in quartz veining and associated stockworks. As of March 2010 the property contained a 43-101-compliant resource of 3.1 million oz of gold (two-thirds of which are counted in probable reserves) and 25.0 million oz of silver. Put another way there are indicated resources of 13.8 million tonnes averaging 6.59 g/t AuEq and inferred resources of 5.0 million tonnes averaging 3.56 g/t AuEq.

All that is fine and good, but it will cost Goldcorp more than its original $3.6-billion investment to create a mine and plant. The feasibility study puts the total preproduction cost at $274.9 million for a project with a mine life of 10 years. The venture will produce up to 285,000 oz of gold per year at a average cash cost of $60.00/oz. The extremely low gold production cost makes Cerro Negro extra attractive.

Confronted with Goldcorp's deeper pockets, Eldorado could do nothing but withdraw its offer on Sept. 7, only five days after it confirmed an offer had been made. This might be the shortest contested takeover in Canadian mining history.

They with the fattest wallet win again. That happens regularly - Xstrata swallowed Falconbridge, Vale scooped up Inco, Teck bought out its coal partners, and in dozens of other deals since then.

I have a little corner in the back of my mind that makes me want to see other factors besides shareholder greed considered in corporate takeovers. I still believe the merger of Falconbridge and Inco would have created a uniquely Canadian nickel powerhouse. I would like to see more Canadian assets in Canadian hands. But that is just one opinion, and it doesn't change the past.

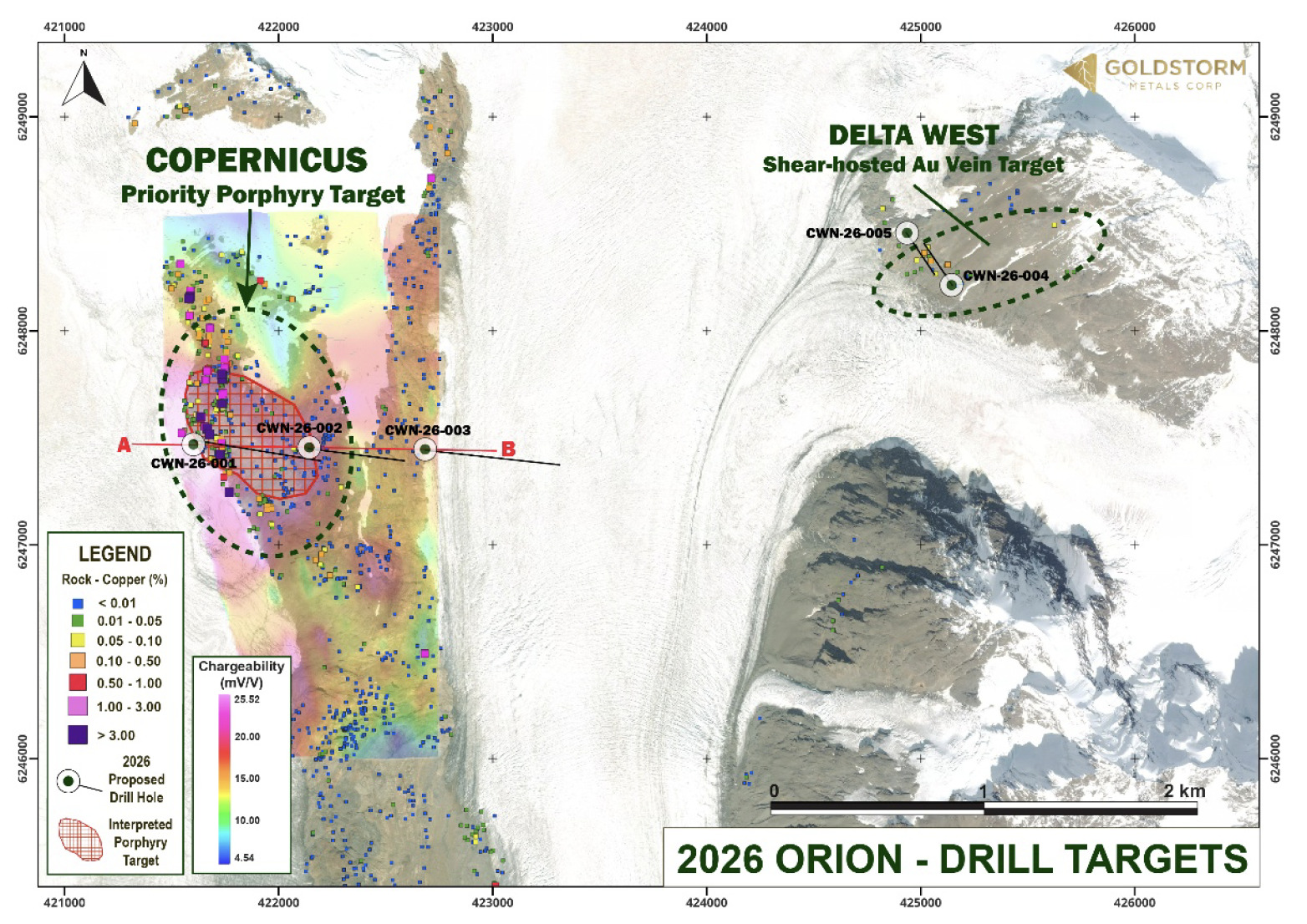

May 27, 2026

Comments