SASKATCHEWAN – The newly completed preliminary economic assessment for the Muskowekwan potash mine notes a 20% increase in production potential, to 3.4 million t/y, according to

Amec Foster Wheeler that produced the report.

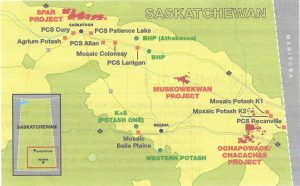

[caption id="attachment_1003718745" align="alignleft" width="300"]

Location of the Muskowekwan project relative to other potash mines in Saskatchewan. Credit: Encanto Potash.

Location of the Muskowekwan project relative to other potash mines in Saskatchewan. Credit: Encanto Potash.[/caption]

The mine is a joint venture of Vancouver’s

Encanto Potash and the

Muskowekwan First Nation. (See the June/July 2017 issue of

CMJ for information about the historic agreement that makes this possible.) Encanto has already signed offtake agreements for 5.0 million t/y for 20 years with customers in India.

The increase in output is due to greater processing plant capacity. And that production rate could be maintained for 48 years, according to the PEA. The initial capital expenditure – with an accuracy of –30% to +50% – would total $3.73 billion including a contingency of $568 million.

Encanto has also updated its 2013 prefeasibility study mining plan that was originally designed for 2.8 million t/y. The 3.4-million-t/y PEA envisions both primary and secondary solution mining with possible production efficiencies. Proven and probable reserves for the Muskowekwan mine total 670.84 million tonnes grading 24.14% potassium chloride and containing 161.98 million tonnes of KCl are sufficient to support either scenario.

The PEA puts the pre-tax net present value at $1.13 billion with a 10% discount rate ($860 million after taxes) and the internal rate of return at 18.9% (17.9% after taxes). Encanto said in a release that the economic model is based on financing of 80% of the capital at a 20-year amortization to match the 20-year offtake agreement.

More information about the Muskowekwan project is posted at

www.EncantoPotash.com.

Comments